Understanding wine distribution for premium collectors

Buying premium or limited edition wines seems simple: find a bottle you want, purchase it, and enjoy. Yet behind every cellar-worthy vintage lies a complex distribution network that shapes availability, pricing, and accessibility. For collectors seeking rare bottles at fair prices, understanding how wine collection reaches the market is crucial. This guide explains the systems that govern wine distribution, from traditional three-tier models to modern direct-to-consumer channels, revealing how rebellious brands leverage scarcity and storytelling to create desirability whilst helping you navigate smarter buying strategies.

Table of Contents

- Key takeaways

- The three-tier system: foundation of US wine distribution

- Comparing wine distribution: Europe’s multichannel strategies

- Current trends: direct-to-consumer sales and premium wine dynamics

- Leveraging limited editions and rebellious brand ethos in wine distribution

- Explore premium and limited-edition wines at FU Wine

- Frequently asked questions about wine distribution

Key Takeaways

| Point | Details |

|---|---|

| Three tier dominance | The US three tier system separates producers, distributors and retailers, shaping pricing and availability. |

| Direct to consumer importance | Direct to consumer channels are key for premium wines, offering access beyond traditional retail. |

| Limited editions storytelling | Limited editions use selective distribution and storytelling to boost desirability among collectors. |

| Navigate channels for buying | Understanding regulatory differences and channel options helps buyers source rare wines at fair prices. |

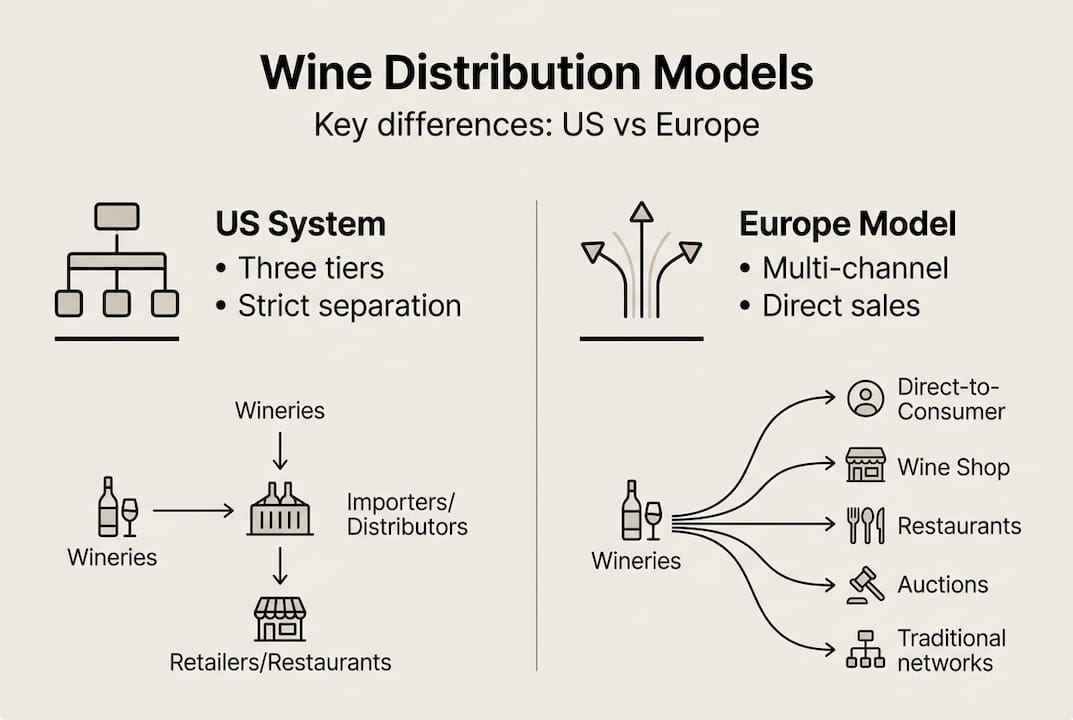

The three-tier system: foundation of US wine distribution

The US wine distribution primarily operates under a three-tier system: producers and importers form the first tier, distributors and wholesalers the second, and retailers the third. This structure emerged after Prohibition ended in 1933, designed to regulate alcohol sales, collect taxes efficiently, and prevent monopolistic control. The system mandates strict separation, prohibiting cross-ownership between tiers to maintain independence and accountability.

Each tier serves a specific function. Producers create wine and sell to licensed distributors. Distributors purchase inventory, warehouse products, and sell to retailers whilst handling logistics and compliance. Retailers operate shops, restaurants, or tasting rooms where consumers make final purchases. This separation ensures regulatory oversight at multiple checkpoints but creates inefficiencies that affect pricing and availability.

The three-tier model presents challenges for premium and limited-edition wines:

- Multiple markups inflate retail prices as each tier adds margin

- Distributors prioritise high-volume brands over boutique producers

- Geographic fragmentation limits availability across state lines

- Smaller producers struggle to secure distribution contracts

- Collectors face difficulty accessing rare allocations through retail channels

Exceptions exist within this framework. Control states like Pennsylvania and Utah operate government-run wholesale or retail operations, adding another layer. Some states permit self-distribution, allowing small producers to sell directly to retailers without a middleman. Wineries can also operate tasting rooms for on-site sales, creating direct-to-consumer touchpoints that bypass traditional distribution entirely.

“The three-tier system was built for control and tax collection, not efficiency or consumer access to premium wines.”

Despite exceptions, the three-tier system remains dominant across most US markets. This creates pricing pressure and availability gaps that affect collectors seeking rare bottles. Understanding these structural limitations helps explain why premium wines often cost significantly more in traditional retail channels compared to direct-to-consumer or international markets. For collectors, recognising how the system works reveals opportunities to source better wines through alternative channels that avoid multiple distribution markups.

Comparing wine distribution: Europe’s multichannel strategies

European wine distribution operates differently, embracing multichannel strategies that provide producers with flexibility and consumers with better access. In Europe and Germany, wine distribution emphasises multichannel approaches: direct-to-consumer accounts for 28% of distribution share, gastronomy represents 24%, and food retail captures significant volume. Most producers actively use two to four channels simultaneously, with cluster analysis identifying focused, diversified, and broad distribution strategies based on business goals.

This multichannel model contrasts sharply with US three-tier rigidity. European producers can sell directly to consumers through cellar doors, online platforms, and wine clubs whilst simultaneously distributing through wholesalers to restaurants and retail shops. This flexibility allows producers to maintain control over brand positioning, capture higher margins through direct sales, and gather valuable consumer data that informs production and marketing decisions.

The following table compares key differences between US and European distribution approaches:

| Aspect | US three-tier system | European multichannel model |

|---|---|---|

| Structure | Mandatory separation of producers, distributors, retailers | Flexible combination of direct, wholesale, retail, gastronomy |

| Producer control | Limited; must work through distributors | High; can choose multiple channels simultaneously |

| Pricing | Multiple markups inflate retail prices | Direct channels reduce markups, improving value |

| Consumer access | Geographic limitations, allocation barriers | Broader access through diverse touchpoints |

| Data insights | Minimal producer visibility into consumer preferences | Direct channels provide rich consumer data |

| Premium wine focus | Distributors favour high-volume brands | Producers can target niche collectors directly |

Direct-to-consumer channels prove particularly valuable for premium and limited-edition wines. Producers maintain direct relationships with collectors, offering exclusive allocations, personalised service, and storytelling that builds brand loyalty. The wine trade guide demonstrates how specialised retailers and direct channels complement each other, creating a robust ecosystem that serves diverse consumer preferences.

Pro Tip: Collectors seeking premium wines should explore multichannel purchasing strategies. Combine direct winery purchases for allocations and exclusives with selective retail relationships for immediate access and diverse inventory. This approach mirrors European flexibility, maximising access to rare bottles whilst optimising price points.

Multichannel distribution also benefits producers strategically. Focused strategies concentrate on one or two channels, ideal for small boutique wineries targeting collectors. Diversified approaches balance direct sales with selective wholesale, capturing different market segments. Broad strategies utilise all available channels, suitable for larger producers with varied product ranges. Each strategy reflects different business priorities, production scales, and target audiences.

For collectors, understanding these multichannel dynamics reveals why European wines often offer better value and accessibility. Producers can bypass intermediaries, reducing costs and maintaining quality control. Direct relationships enable storytelling and education that enhance appreciation and justify premium pricing. This model demonstrates how distribution structure directly impacts collector experience, availability, and pricing for limited-edition and premium wines.

Current trends: direct-to-consumer sales and premium wine dynamics

Direct-to-consumer wine sales face significant headwinds, yet premium wines demonstrate remarkable resilience. US DTC wine shipments declined 15% in volume to 5.4 million cases and 6% in value to $3.7 billion in 2025, now representing 7% of the off-premise market compared to 12% in 2021. However, average bottle price rose 11% to $56.78, driven by a mix shift away from lower-priced wines as consumers prioritise quality over quantity.

This trend reveals a bifurcated market. Volume declines reflect broader economic pressures and changing consumer habits, but premium wines maintain strong demand amongst collectors willing to invest in quality. Premium West Coast wineries in the top quartile with 64% DTC sales grew revenue 21% from 2022 to 2024, whilst the overall industry experienced negative 2% revenue growth. Wineries with greater than 70% DTC sales showed 6.1% revenue growth, demonstrating the power of direct channels for premium positioning.

Several factors drive these divergent outcomes:

- Economic uncertainty reduces discretionary spending on everyday wines but collectors maintain budgets for premium and limited editions

- Shipping cost increases and regulatory complexity create friction for lower-margin DTC transactions

- Premium wineries leverage tasting rooms, wine clubs, and exclusive allocations to build loyal collector bases

- Brand storytelling and scarcity tactics amplify desirability for high-end bottles, justifying premium pricing

- Smaller producers benefit from self-distribution and direct sales, avoiding distributor margins and maintaining control

For collectors, these trends create opportunities. As mainstream DTC volume declines, premium producers focus resources on high-value customers through personalised service, exclusive releases, and curated experiences. Tasting room visits and wine club memberships provide access to limited allocations unavailable through retail channels. Direct relationships with producers enable collectors to secure rare bottles at prices that reflect production costs rather than multiple distribution markups.

“Premium wine collectors drive DTC growth by prioritising quality, exclusivity, and direct producer relationships over convenience and low prices.”

Pro Tip: Focus your collecting strategy on wineries with strong DTC programmes and limited production. Join wine clubs offering allocation access, visit tasting rooms for exclusive releases, and build relationships with producers who prioritise quality over volume. This approach positions you to access the best wines at fair prices whilst supporting producers who invest in craftsmanship.

The shift towards premium DTC sales also reflects changing collector preferences. Modern wine enthusiasts value transparency, authenticity, and storytelling alongside quality. They seek connections with producers who share their values and offer unique experiences beyond the bottle. This dynamic favours rebellious brands that challenge industry norms, deliver exceptional value, and create emotional engagement through compelling narratives and limited-edition releases.

Understanding these market dynamics helps collectors navigate distribution channels strategically. Premium wines remain resilient through direct channels despite broader market challenges, creating a favourable environment for those who prioritise quality and exclusivity. By focusing on DTC relationships and selective retail partnerships, collectors can access rare bottles whilst avoiding the inefficiencies and markups inherent in traditional three-tier distribution.

Leveraging limited editions and rebellious brand ethos in wine distribution

Limited-edition wines and rebellious branding transform distribution from a logistics exercise into a strategic tool for creating desirability and collectibility. Rebellious brands like 19 Crimes use limited-edition labels for storytelling and impulse purchases via retail, whilst Rebellium hand-paints magnums for collectors at $2,000 to $7,000. Cult wines like Screaming Eagle produce only 1,000 cases annually, using allocations and waitlists to amplify exclusivity and demand.

Limited editions for premium wines create scarcity and collectibility, ideal for market entry in high-impulse channels like travel retail. This strategy proves effective for beverages and spirits through numbered bottles, unique packaging, and compelling storytelling that connects emotionally with collectors. Distribution becomes selective rather than broad, reinforcing premium positioning and justifying higher price points.

The following table contrasts standard distribution approaches with limited-edition strategies:

| Element | Standard distribution | Limited-edition distribution |

|---|---|---|

| Production volume | High volume for broad availability | Deliberately constrained for scarcity |

| Channel selection | Wide retail distribution | Selective doors, DTC, travel retail |

| Pricing strategy | Competitive pricing for volume | Premium pricing justified by exclusivity |

| Marketing approach | Brand awareness and accessibility | Storytelling, numbered bottles, allocations |

| Consumer engagement | Transactional purchase | Emotional connection, collectibility |

| Availability | Consistent stock levels | Time-limited releases, waitlists |

Limited editions deliver multiple benefits for collectors and producers:

- Scarcity drives urgency and perceived value, encouraging immediate purchase decisions

- Unique packaging and storytelling create emotional connections beyond the liquid itself

- Selective distribution through premium channels reinforces quality positioning

- Numbered bottles and certificates of authenticity enhance collectibility

- Allocations and waitlists build anticipation and community amongst enthusiasts

- Higher margins enable producers to invest in quality and craftsmanship

Rebellious brands amplify these dynamics by challenging industry conventions. They reject pretentious pricing, question traditional gatekeeping, and speak directly to collectors tired of paying inflated prices for labels and status. This ethos resonates with modern consumers who value authenticity, transparency, and exceptional quality over heritage and prestige. By combining limited-edition scarcity with rebellious positioning, brands create powerful narratives that drive demand and loyalty.

Pro Tip: Identify limited-edition releases by following producers on social media, joining mailing lists, and building relationships with selective retailers who receive allocations. Act quickly when releases are announced, as scarcity creates rapid sell-outs. Prioritise producers whose rebellious ethos and quality focus align with your collecting philosophy.

Direct-to-consumer channels prove essential for limited-edition distribution. Producers maintain control over allocations, ensuring bottles reach true collectors rather than speculators. Wine clubs and mailing lists provide early access to releases, rewarding loyal customers with exclusive opportunities. Tasting rooms offer personalised experiences where collectors can taste, learn, and purchase limited editions directly from the source.

Travel retail and selective wholesale partnerships complement DTC strategies. High-impulse channels like airport duty-free shops capture collectors during travel, when they are receptive to premium purchases and unique discoveries. Selective retail partnerships with specialised exclusive wine releases doors ensure limited editions reach knowledgeable staff who can tell the story and connect with the right customers.

For collectors, understanding how limited editions and rebellious brands leverage distribution reveals opportunities to access rare wines at fair prices. By engaging directly with producers, joining allocation lists, and supporting brands that challenge industry norms, you position yourself to discover exceptional bottles that combine quality, scarcity, and compelling narratives. This approach transforms collecting from passive purchasing into active participation in a community that values craftsmanship, authenticity, and rebellion against inflated pricing.

Explore premium and limited-edition wines at FU Wine

Now that you understand how wine distribution shapes availability and pricing, it’s time to experience these principles in action. FU Wine embodies the rebellious ethos and premium quality discussed throughout this guide, offering collectors access to rare and limited-edition wines at prices that reject industry markups and pretentious positioning.

Our premium wine collection features carefully curated bottles that combine exceptional quality with genuine value. From cellar-aged treasures like the F.U. Barossa premium cabernet to fresh releases such as the Fu Barossa Valley pinot noir, every wine reflects our commitment to sourcing premium bottles that collectors deserve without the inflated prices they don’t. We leverage direct relationships, opportunistic buying, and a rotating deal-driven model to deliver scarcity and desirability at accessible price points. Explore our collection today and discover wines that prove premium quality shouldn’t require pretentious pricing.

Frequently asked questions about wine distribution

What is the three-tier wine distribution system?

The three-tier system separates producers, distributors, and retailers into distinct tiers with no cross-ownership allowed. Established after Prohibition in the US, it regulates alcohol sales and tax collection but creates multiple markups that inflate retail prices for premium wines.

How does direct-to-consumer wine sales work?

Direct-to-consumer sales allow wineries to sell bottles directly to consumers through tasting rooms, wine clubs, and online platforms, bypassing distributors and retailers. This approach reduces markups, enables producer-consumer relationships, and provides access to limited allocations unavailable through traditional retail channels.

What makes limited-edition wines valuable?

Limited editions create scarcity through constrained production, unique packaging, and selective distribution that amplify collectibility and desirability. Numbered bottles, compelling storytelling, and time-limited availability drive urgency whilst premium positioning justifies higher prices amongst collectors seeking exclusivity.

Can collectors buy premium wines outside traditional retail?

Yes, collectors can access premium wines through direct-to-consumer channels including winery tasting rooms, wine club memberships, allocation lists, and online platforms. These alternative channels often provide better pricing, exclusive releases, and direct producer relationships that enhance the collecting experience beyond traditional retail.

How do rebellious wine brands stand out in distribution?

Rebellious brands challenge industry norms by rejecting pretentious pricing, leveraging storytelling and scarcity, and using selective distribution to create emotional connections with collectors. They prioritise direct-to-consumer channels, limited-edition releases, and transparent value propositions that resonate with consumers tired of inflated prices and traditional gatekeeping.