Role of middlemen in wine: pricing and access explained

TL;DR:

- Middlemen in wine distribution are legally required licensed intermediaries controlling product movement, pricing, and availability. They create compounded markups that raise a wine’s retail price from $10 at the winery to as much as $22, limiting consumer access to smaller producers. Understanding their role helps consumers bypass system flaws by seeking direct sales and specialist importers for better prices.

Middlemen in wine distribution are licensed intermediaries who sit between producers and retailers, controlling the movement, pricing, and availability of almost every bottle you buy. In most major markets, their role is not optional. It is legally required. Understanding the role of middlemen in wine means understanding why a $10 bottle at the winery gate can cost $22 on a bottle shop shelf, and why some of your favourite small producers seem to vanish from the market entirely. This is the system that shapes what you drink, what you pay, and what you never get to try.

What is the role of middlemen in wine distribution?

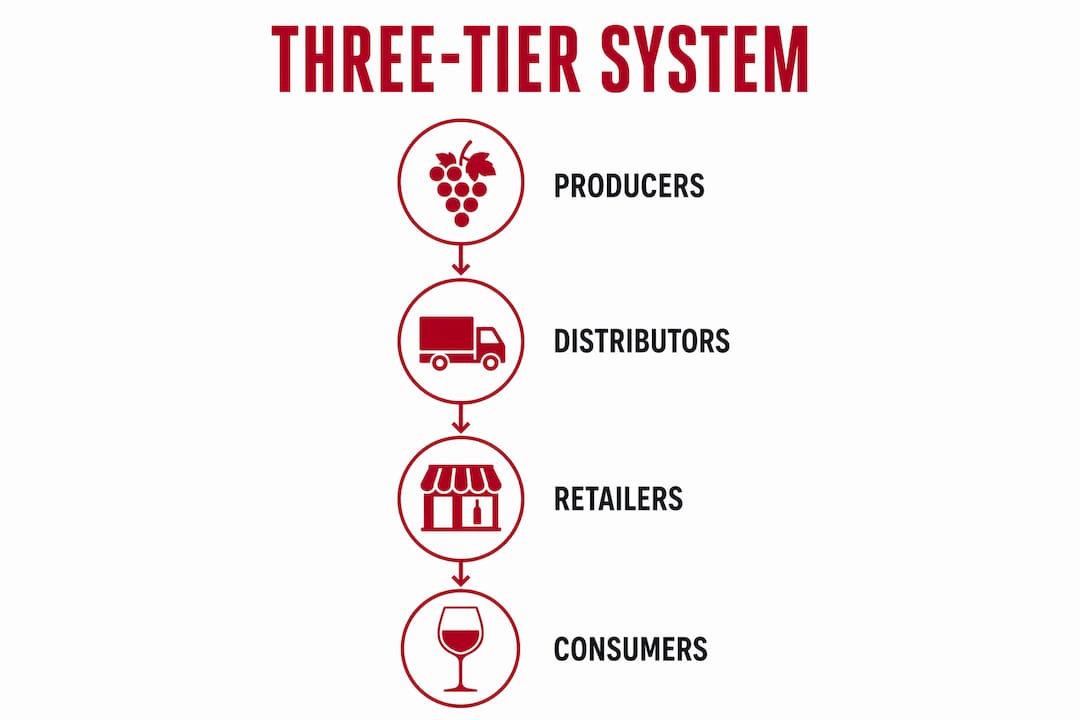

Middlemen in the wine industry are formally known as licensed distributors or wholesalers. They occupy the middle tier of a legally structured supply chain that separates producers, distributors, and retailers into distinct, regulated roles. In the United States, this is called the three-tier system, and it governs how wine moves from winery to glass.

The system exists for regulatory control, not just commercial convenience. After Prohibition, US lawmakers designed the three-tier model to prevent any single entity from controlling production, distribution, and retail simultaneously. That separation is still enforced today. Middlemen are not just useful. In most US states, they are mandatory.

Australia operates differently, with fewer legal mandates around distribution tiers, but the commercial reality is similar. Distributors and importers still control the majority of wine reaching retail shelves, and their decisions about which wines to carry shape what consumers can actually buy.

How does the three-tier system legally structure wine intermediaries?

The three tiers are producers or importers, licensed distributors, and retailers. Each tier is legally distinct. Tied-house laws prevent any one tier from owning or controlling another, which means a winery cannot own a distributor, and a distributor cannot own a bottle shop. The arms-length structure is the point.

This legal separation makes middlemen structurally indispensable in most US states. Producers cannot legally ship directly to retailers or restaurants in the majority of states. They must go through a licensed distributor. That single rule embeds the middleman’s role into every transaction.

Self-distribution is permitted in roughly a dozen US states, but mostly for small producers operating under volume caps. For any winery with national ambitions, a distributor relationship is not a choice. It is a legal prerequisite.

Pro Tip: If you are a small producer or a buyer working with boutique wineries, check whether the producer’s home state permits self-distribution. It can open direct purchasing options that bypass the standard markup chain entirely.

Regional variations matter. Some states allow direct-to-consumer shipping, which lets wineries sell online directly to drinkers. But most retailers still cannot buy directly from wineries, regardless of state. The middleman remains the gatekeeper for the commercial trade.

What impact do middlemen have on wine pricing?

The pricing impact of wine distribution intermediaries is direct and compounding. A winery might sell a bottle at $10 wholesale. A distributor applies a markup of 25–50%, bringing the price to roughly $12.50–$15. A retailer then adds a further 30–50%, pushing the shelf price to $18–$22. A restaurant applies a 2.5x to 3x markup on top of that for by-the-glass pricing.

That cascade effect means a $10 winery price becomes a $22 retail bottle before anyone has poured a drop. Each percentage markup applies to the already-marked-up price, not the original. The compounding is the problem.

Tariff changes make this worse. A 2019 European tariff study showed that retail prices lag tariff or cost changes by over 12 months. Each tier in the chain posts prices on its own schedule, and percentage-based markups amplify the original cost increase before it reaches the consumer. A 10% tariff at the border does not show up as 10% at the shelf. It shows up as significantly more, and later than expected.

Here is how the markup chain typically stacks up:

- Winery wholesale price: The base price, often $8–$15 for a mid-range bottle.

- Distributor markup (25–50%): Applied to the wholesale price, this is the first compounding layer.

- Retailer markup (30–50%): Applied to the distributor’s price, not the original winery price.

- Restaurant markup (2.5x–3x): The final multiplier, applied to the retailer’s cost for by-the-glass pricing.

Understanding what drives wine prices helps you spot where the value disappears in the chain.

How do middlemen influence wine selection and availability?

Distributor decisions about which wines to carry directly determine what appears on retail shelves. This is where the role of intermediaries in wine becomes most consequential for consumers and small producers alike.

Pay-for-performance (PFP) compensation is the dominant model for distributor sales reps in the US. Under PFP, reps earn bonuses based on sales of specific brands, funded by supplier promotional budgets. The result is predictable. Large wholesalers prioritise incentive-paying SKUs, and wines without promotional budgets become effectively invisible to sales reps, even when they are physically in the warehouse.

Small and boutique producers rarely have the budget to compete with large brands for rep attention. Their wines sit in a distributor’s warehouse but never get pitched to buyers. This structural shift reduces the sales expertise devoted to niche wines and shrinks the visible marketplace for consumers.

The concentration of market power compounds this problem. Two firms control about 53% of the US distribution market, and the top 10 firms control over 81%. That concentration means fewer gatekeepers making decisions about which wines reach consumers. A small Barossa producer trying to break into the US market is not just competing for shelf space. They are competing for the attention of a handful of dominant distributors.

- Large national distributors prioritise volume brands with promotional budgets.

- Regional distributors often carry more diverse portfolios but have limited geographic reach.

- Boutique importers specialise in small producers but lack the sales infrastructure of national players.

- Niche wines without distributor champions rarely reach mainstream retail, regardless of quality.

Pro Tip: If you are hunting for wines from small producers, seek out specialist importers and boutique distributors rather than relying on mainstream bottle shops. They carry the wines that never make it into the big distributor catalogues.

Understanding why some wines are hard to find comes down to exactly this: distributor incentives, not wine quality, determine what reaches the shelf.

What are the challenges and benefits of middlemen in the wine industry?

Middlemen provide genuine operational value. They handle warehousing, cold-chain logistics, compliance with state and federal regulations, and the administrative burden of licensing. For a small winery without the resources to manage multi-state compliance, a distributor is not just useful. It is the only practical path to market. Importers and distributors also provide market expertise, buyer relationships, and sales coverage that producers cannot replicate independently.

The challenges are real and structural. Market concentration, PFP incentives, and compounding markups create a system that consistently favours large brands over quality producers and inflates prices for consumers.

| Factor | Benefit | Challenge |

|---|---|---|

| Compliance and licensing | Distributors manage complex multi-state regulatory requirements | Adds cost and dependency for producers |

| Logistics and warehousing | Professional cold-chain storage and delivery | Markup applied at each logistics stage |

| Market access | Established buyer relationships open retail doors | Small producers compete for limited rep attention |

| Pricing transparency | Standardised pricing structures exist across tiers | Compounding markups obscure true winery cost |

| Market concentration | Efficient national distribution for large brands | Two firms control 53% of US distribution, limiting options |

The pricing cascade is the most visible challenge for consumers. The compliance and logistics value is real, but it does not justify the full extent of compounding markups in a concentrated market. For producers, the trade-off is access versus margin. For consumers, it is availability versus price.

Key takeaways

Middlemen in wine are legally mandated intermediaries whose compounding markups, incentive structures, and market concentration directly determine what you pay and what you can actually buy.

| Point | Details |

|---|---|

| Legal mandate | Three-tier laws in most US states make licensed distributors a legal requirement, not a commercial choice. |

| Compounding markups | A $10 winery price becomes $18–$22 at retail after distributor and retailer markups stack. |

| Incentive distortion | Pay-for-performance compensation pushes reps toward big brands, making niche wines invisible despite availability. |

| Market concentration | Two firms control 53% of US distribution, reducing options for small producers and limiting shelf diversity. |

| Price lag | Retail prices reflect tariff and cost changes with a delay of over 12 months due to tiered posting schedules. |

The uncomfortable truth about wine distribution

I have spent years watching the wine industry explain away its pricing with talk of terroir, tradition, and prestige. The reality is more mundane. The biggest driver of what you pay at retail is not the quality of the wine. It is the structure of the distribution system and the incentives baked into it.

The three-tier model made sense after Prohibition. It prevented monopolistic control and kept the trade honest. But the consolidation that has happened since, with two distributors controlling more than half the US market, has turned a regulatory safeguard into a commercial chokehold. Small producers with genuinely exceptional wine get buried because they cannot fund a rep’s bonus. Large brands with mediocre wine get prime shelf placement because they can.

What I find most telling is the price lag issue. Consumers absorb amplified tariff costs months after the fact, with no visibility into why their favourite bottle suddenly costs more. The system is not designed for transparency. It is designed for compliance and control.

For wine enthusiasts, the practical implication is clear. If you want access to quality without paying for the full markup cascade, you need to go around the system where you legally can. Seek out direct-to-consumer wineries in states that permit shipping. Find specialist importers who champion small producers. And pay attention to platforms that source outside the standard distributor chain.

The middleman is not going away. But understanding how the system works is the first step to not overpaying for it.

— Damien

Premium wine without the markup chain

Every bottle at Com has been sourced to cut through the layers that inflate what you pay at a standard bottle shop.

Com works directly with producers, distressed inventory releases, and allocation channels to bring you rare and premium wines at prices the standard distribution chain simply cannot match. Think 30–70% below typical retail on bottles that are genuinely hard to find. No inflated prestige pricing. No rep incentive markups buried in the shelf price. Just quality wine at a price that makes sense. Browse the current offers and see what the system has been keeping from you.

FAQ

What is the three-tier system in wine distribution?

The three-tier system is a legally mandated structure separating wine producers, licensed distributors, and retailers into distinct regulated roles. Tied-house laws prevent any tier from owning or controlling another, making distributors a legal requirement in most US states.

How much do middlemen add to the price of wine?

Distributors typically add a markup of 25–50% and retailers add a further 30–50%, turning a $10 winery wholesale price into an $18–$22 retail bottle before restaurant markups apply.

Why do some wines disappear from shelves?

Pay-for-performance compensation means distributor sales reps focus on brands with the largest promotional budgets. Wines without supplier incentive funding become invisible to reps, even when physically available in the warehouse.

Can wineries sell directly to consumers without a middleman?

Direct-to-consumer sales are permitted in some states, but self-distribution is only available in roughly a dozen US states and mostly for small producers under volume caps. Most retailers still cannot buy directly from wineries by law.

Does market consolidation affect wine choice?

Two firms control about 53% of the US distribution market and the top 10 control over 81%. That concentration limits which wines reach retail shelves and reduces the leverage small producers have in negotiating distribution deals.